Your Guide to Obtaining a Credit Score and Full Credit Report

Checking your credit score and your full credit report in a regular manner is important if you want to apply for a loan, mortgage or apartment.

It is also important if you are applying for a new job, as employers have the right to check your credit. Knowing your score will give you a better idea of how much credit you may qualify for.

Furthermore, monitoring your report and credit activity is a preventative measure for identity fraud.

A credit report is different from a score because it lists your full credit history. This history includes the number of credit lines you have open, how often you pay back your debt on time and whether you have filed for bankruptcy or gone through foreclosure.

A credit score, on the other hand, may not give you as detailed information and usually comes from just one of the three major credit bureaus.

You may receive credit scores and credit reports for free by contacting the right companies or requesting reports from the correct website. You also have the option, however, of purchasing additional credit reports from each of the major companies.

What You Should Know About the Three Reporting Companies

There are three credit reporting companies that most U.S. lenders use to check your score: Equifax, Experian and TransUnion. If you are a credit card, loan or mortgage applicant, it is likely that you have already checked your score with data provided by one of these three companies.

Each of these credit bureaus will collect certain information about you to determine your score and develop your report.

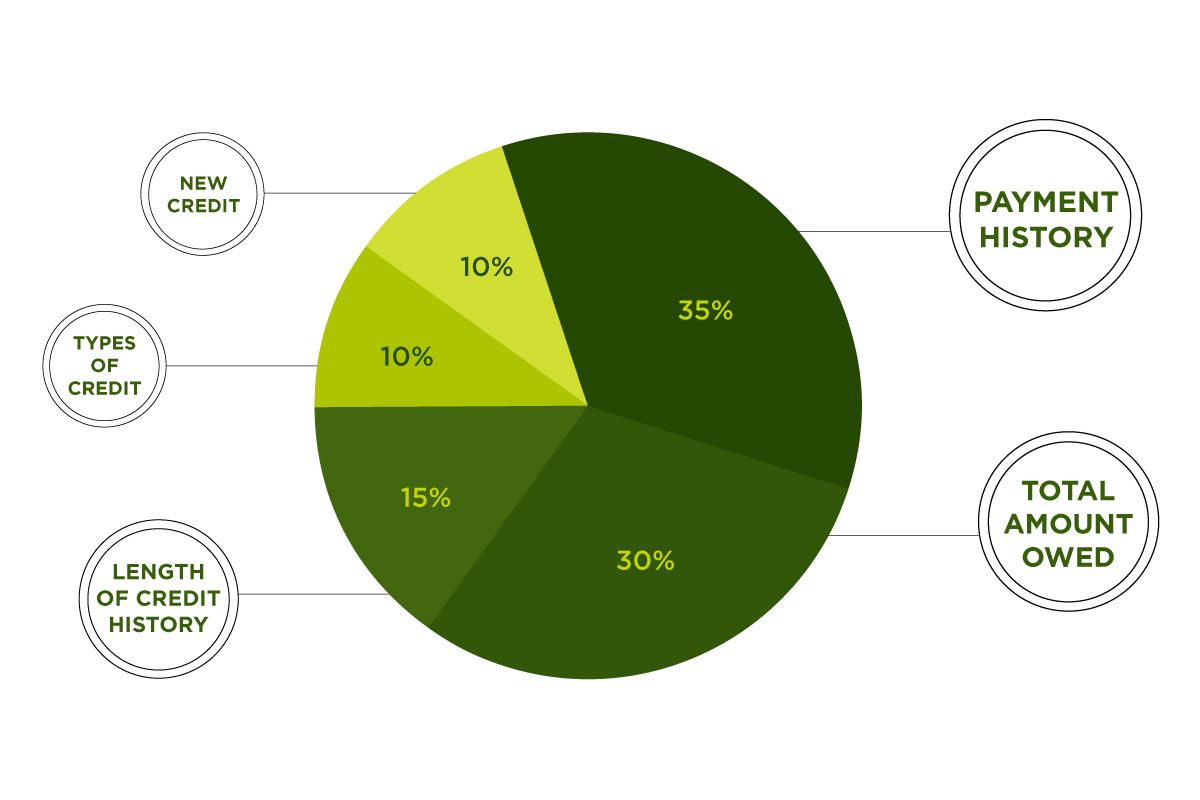

The information that impacts your score includes your payment history, the debt you owe versus the amount of credit available to you, the length of your credit history, the number of accounts you have open and what types of debt you have.

In general, your payment history is the most important aspect of your report. This is because it gives lenders the best prediction of how often you will pay your bills on time.

While every reporting company gathers similar information on your credit, each one uses its own formula to calculate a report.

Consequently, a report from one company may look very different from that of another company. You may also find errors on one report that do not appear on another.

Furthermore, a lender who checks your score may use only one company’s data or it may use data from all three credit bureaus. Thus, it is important for you to check your score with all three companies.

You may receive a free copy of your credit report from Equifax, Experian and TransUnion once per year. If you go above this allotment, you may be required to pay a fee. Keep in mind that reports are not offered directly through each individual company, but through one website.

When and Where to Obtain Your Free Credit Report

Once every 12 months, you are entitled to one free credit report that gives you information from the three major reporting companies. Alternatively, you may order one report from each company once a year, instead of receiving them all at once.

You may qualify for an additional report if you have recently been denied by a lender, are unemployed, receive welfare or are unfortunately experiencing identity theft.

If one or more of these circumstances applies to you, must put in your request before 60 days have passed. Requesting a report at any other time, after you have received the maximum number of reports for the year, will result in a fee.

The Annual Credit Report website is the only site authorized by the federal government to distribute credit reports.

On the site, you may request one report at a time or all three at once. You may want to stagger the reports if you want to monitor your score on a more regular basis.

If you are applying for a very large sum of money, however, you may want to receive all three reports at the same time so that you know exactly what credit information your lender will see.

Submitting a request for a report requires you to provide certain personal information. For instance, you will need to enter your name, address, Social Security Number (SSN) and date of birth.

The Annual Credit Report site may also prompt you to answer questions about your loans, mortgage payments or other applicable debts in order to prove your identity.

If you wish to buy additional copies of your reports, contact Equifax, Experian and TransUnion directly by telephone.

This option may benefit you if you feel the need to monitor your reports as closely as possible. The fee for each report may vary.

You may also contact each of the agencies for a number of other inquiries you may have including:

- disputes you may see on your report

- fraud alerts

- security freezes

- to learn more about their products and services

- or to answer any other questions or concerns you may have regarding your report

How to Contact the Credit Bureaus

Why it is Important to Monitor Your Credit Report

Keeping an eye on your credit report will give you a better chance of spotting errors in your personal information and credit history.

If your information is incorrect or needs to be updated, you may contact any of the three reporting companies or submit your update through the Annual Credit Report website.

A credit report can also be used to see what lines of credit you have open so that you can learn how to consolidate your debt most effectively.

You may need to update your information if you have recently gotten married, moved to a new home or went through a similar life change.

It is also important to manage your credit score if you are interested in government housing grants or other loan options.

Monitoring your report will also give you a better chance of combating identity fraud. An identity thief steals your SSN and banking information to apply for a new credit card under your name. He or she may then use the new card to withdraw large sums of money or make expensive purchases.

This may result in a significant drop in your credit score and hurt your chances of receiving approval for future loans.

If you notice the signs of identity fraud early on, you may be able to prevent some or all of its negative effects.

Will your credit score be negatively impacted by an inquiry?

Your credit score will not be impacted by soft inquiries, but it will be altered by hard inquiries. Checking your own credit score is considered a soft inquiry.

Potential employers and companies may also order a soft inquiry if you are applying for a job and they want to perform a background check.

Hard inquiries take place when a financial institution, lender or even a rental association wants a detailed explanation of your loan or credit history.

This type of inquiry will lower your credit score by a few points and be recorded on your report. If you undergo multiple hard inquiries in a short period of time, your score may be significantly depleted.

Top 10 tips to keep a high credit score

1. Make sure that you are paying your bills on time

This is probably the most significant factor in making sure your credit score maintains at a healthy number. Although we cannot say for sure exactly how this is worked out on the back end, as the algorithms to calculate the numbers vary and are also guarded, it is estimated that roughly 35% of the score has to do with your payment history.

It is important to note also that if you accidentally miss a payment, you may and should, contact your lender to forgive the late payment. Most people think that they will say no, but you’ll be surprised. Most of them are open to helping out a long-term, loyal customers, especially if your history shows your consistency.

2. Don’t carry an outstanding balance if you can

This is another typical myth that most people are taught – having 30-50% of your credit being used is a good thing. On the contrary, you can definitely pay off your cards in full each month and you will see long term positive results in your score. This also helps you not pay interest on the funds you are utilizing.

3. Set up auto payments

It is very easy to forget to make a payment if you have to physically go in and pay. Setting up online payments is very simmple to do and once done, you need not worry about making a late payment or forgetting to do so altogether. Another perk is you have your online banking as a bookkeeping tool so you can see all your transactions in a quick way.

4. Don’t check your score every month

Typically, it takes a bit of time to see changes on your score. Don’t drive yourself crazy checking it every other day in hopes that it is going up. It is suggested to check it a few times a year, or even quarterly. This will give you the bigger picture on your progress.

5. Take credit limit increases

If a lender offers to increase your credit, take it! This is a sign that you have been a responsible with your spending and they are willing to give you more to utilize.

6. See if your lender will lower your APR

Most people assume that lenders will say no if you ask this. But most of the time they may work with you in order to maintain the good relationship with a loyal customer with excellent credit. The worst thing that can happen is they say no, in which case you are in the same position as before. Try it!

7. Don’t close accounts that are in good standing

Most people think that if you are not using a card, it is better to close the account. Another common misconception is that it’s better to have fewer cards which means that you are a responsible person who does not need 10 different credit cards. Both of these are incorrect. 15% of your credit score is calculated by how long your accounts have been open. Based on this, keep accounts you have in good standing and make sure to use them once in a while!

8. Open accounts only when it makes sense

Although it is enticing to “save 30%” by opening an account on the spot of some of your favorite stores, this is not the ideal scenario you want to use when maintaining your credit score healthy. Make sure you are only utilizing credit for when you know that your checking or savings account will be stretched.

9. Pay off revolving debts first

There are 2 types of debts – installment & revolving. Installment debts are typically fixed loans for a long term. These usually have lower APR. Revolving debts have higher interest and a good example is department store cards.

10. Check your score once a year!

Make sure to check in on your score once a year – its free! Alot of people actually fail to do this and this can sometimes lead to not spotting any discrepancies on your report that may be bringing the score down inadvertently.

Checking it will also allow you to see your progress and where you are with different bureaus. It is good to know where you stand so make sure you are on top of this.

Learn About Useful Credit Calculators

- Debt-to-Income Calculator

- Credit Card Payoff Calculator

- Auto Loan Calculator

- Mortgage Calculator

- Loan Calculator